Published November 24, 2025

Why First-Time Home Buyers Are Older Than Ever and What It Means for Bakersfield’s Housing Market

For the first time in history, the typical first-time home buyer in America is 40 years old.

This insight comes from the newly released National Association of Realtors Profile of Home Buyers and Sellers. This annual report surveys buyers and sellers who completed a home purchase between July 2024 and June 2025. According to the findings, first-time buyers made up only 21% of all home purchases last year. Before 2008, the historical average was closer to 40%. High rent, student loan payments, and a higher cost of living are delaying the path to homeownership and reshaping who can enter the market.

So what does this national trend mean for Bakersfield? And how does it connect to our local home values?

To understand the connection, we need to look at how Bakersfield’s housing market has changed over the last 15 years.

Bakersfield Home Prices Have Climbed Steadily for 15 Years

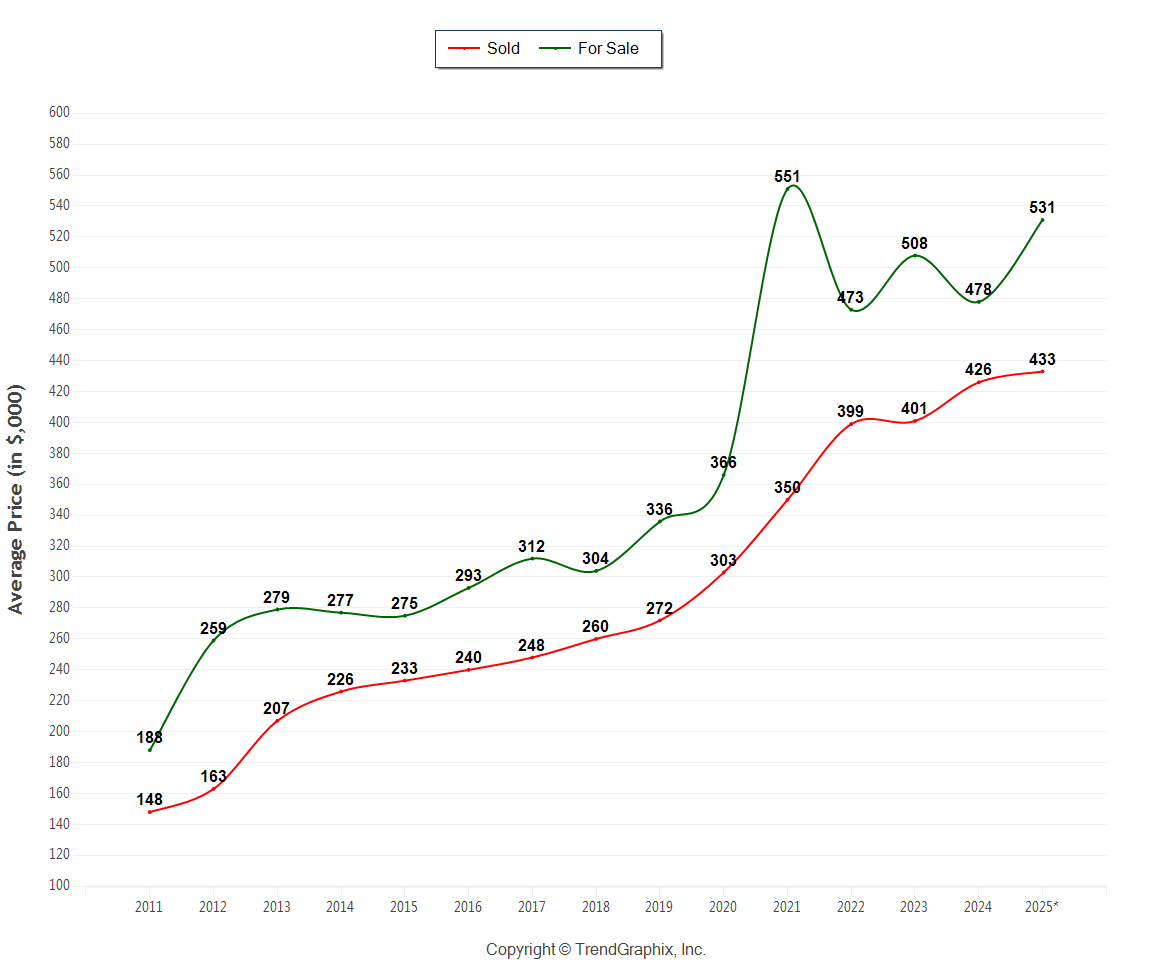

The graph above, pulled from the Golden Empire MLS, shows the average sold price for single family homes in Bakersfield over the last decade and a half. Several clear trends stand out:

-

Bakersfield’s average sold price has increased for 15 straight years.

-

Home values have nearly tripled since 2011.

-

Even with higher interest rates, sold prices have remained stable with only minimal fluctuation.

-

The market has shifted from rapid pandemic era appreciation to steady and sustainable growth.

-

Bakersfield’s affordability continues to attract buyers from higher priced California metros, which helps support demand and home values.

Although we are seeing home values appreciate at a more steady rate, the long-term trend is unmistakable. Bakersfield has experienced consistent and reliable appreciation that many other real estate markets have not.

How This Relates to the Rising Age of First-Time Buyers

Across the country, first-time buyers are entering the market later in life. Three factors play a major role in this shift:

-

High rent makes it difficult to save for a down payment.

-

Student loan debt delays financial readiness.

-

Higher home prices require more cash reserves than in previous generations.

This means many buyers spend years saving before they can consider purchasing. By the time they are ready, they are older and purchasing at higher price points than their parents or grandparents did.

In Bakersfield, this trend aligns with what we see locally. Prices have climbed steadily over the last 15 years. Buyers entering the market today are stepping into a landscape that looks very different from the one young buyers faced in the early 2000s.

Bakersfield Remains One of California’s Most Affordable Entry Markets

Even with ongoing appreciation, Bakersfield continues to offer one of the most attainable price points in the state. This affordability is a major reason why:

-

Many buyers relocate from Los Angeles, Orange County, and the Bay Area.

-

Demand remains steady, even during periods of higher interest rates.

-

Home values have stayed stable while many other areas have experienced volatility.

For local residents, rising prices mean more time spent saving for a down payment. Even so, Bakersfield is still one of the few places in California where first-time homeownership is within reach without needing an unusually high income.

The Bottom Line

National trends show that first-time buyers are older, fewer in number, and facing more financial obstacles than ever before. Locally, Bakersfield’s steady price growth and relative affordability set our market apart from many parts of the state.

Even as prices have risen over the last 15 years, Bakersfield continues to offer one of the most accessible paths to homeownership in California. That is a major reason why demand here has remained strong and why home values continue to hold steady.

If you are thinking about buying or selling and want personalized guidance for today’s market, our team is here to support you. Call or text 661-665-SOLD and we will walk you through your next steps.